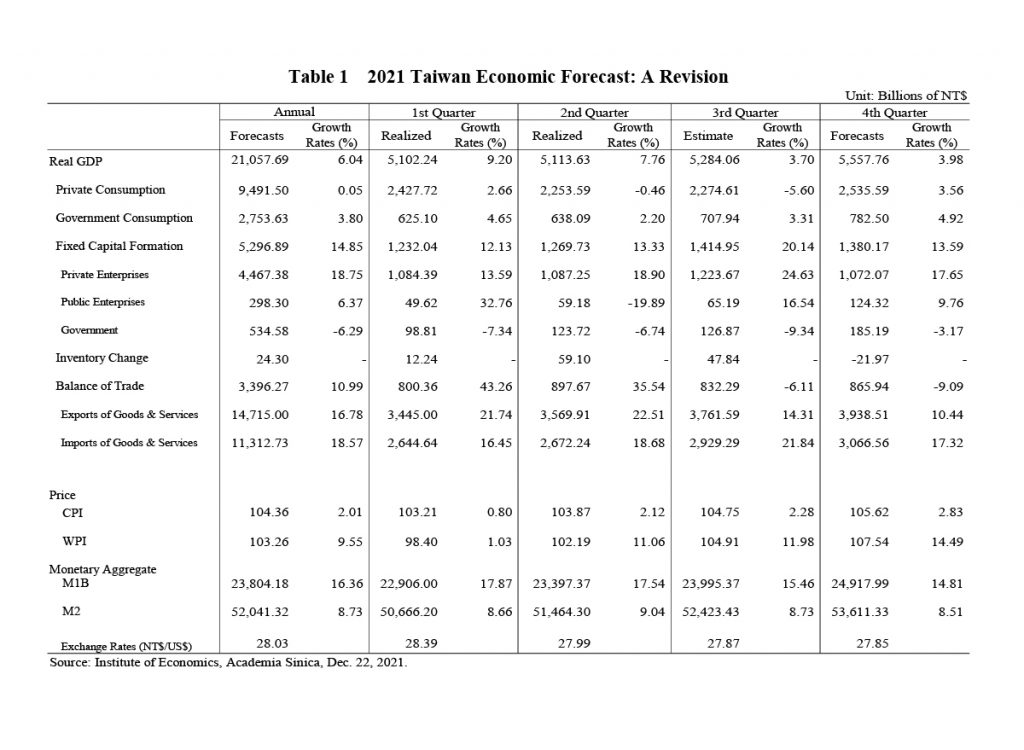

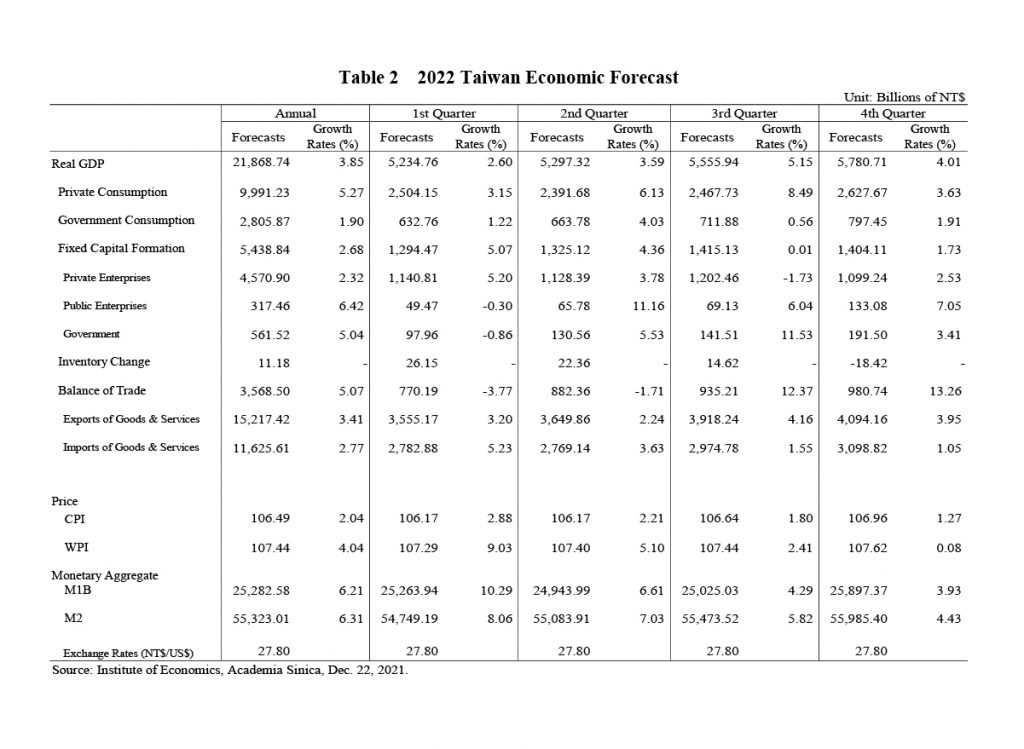

In 2021, the world actively promoted the Covid-19 vaccination, the economy has gradually recovered. Domestically, starting from the end of July, spread of the pandemic slowed down. Furthermore, foreign trade continued to expand, mainly driven by acceleration of infrastructure construction and digital transformation in major countries. Real GDP growth rate in Taiwan in the third quarter reached 3.70% and growth in the year 2021 is expected to be 6.04%. Looking forward to 2022, due to supply chain bottlenecks and inflation risk, foreign demand is expected to slow down. However, with the gradual increase in domestic vaccination rate, consumption is expected to pick up. Considering high base period factors, the real economic growth rate in 2022 is expected to be 3.85%.

Private consumption was affected by the pandemic in the second and third quarters of 2021 as consumption of catering, public transportation, leisure and entertainment, etc. was curtailed. Real private consumption in third quarter of 2021 declined by 5.60%. The fourth quarter is traditionally the purchasing season and owing to effects of the epidemic, market demand has pushed up online shopping. The quintuple stimulus voucher and the issuance of coupons by various ministries are expected to help boost consumption in the forthcoming months. It is estimated that the real private consumption growth rate will increase by 0.05% in 2021. If the effect of the epidemic remains under control, consumer confidence will rebound. Furthermore, the government will raise the basic wage rate and salaries for government employees next year. Real private consumption is expected to rise 5.27% in 2022.

Private investment in technology manufactures such as semiconductors and other related products continues to expand. Besides expansion of capacity in aviation and shipping, telecommunications companies are actively investing in 5G infrastructure. Growth in private investment was of the order of 24.63% in the third quarter. The estimated annual growth in real private investment in 2021 is around 18.75%. Next year, investment for localization of supply chains will continue. It is expected that in 2022, considering the high growth in the base period, real private investment will grow 2.32%. In addition, the government is promoting construction in urban areas and in public green energy facilities. It is expected that fixed capital formation in 2021 and 2022 will grow by 14.85% and 2.68% respectively.

Foreign trade is expanding, growth in exports and imports of goods and services in third quarter of 2021 being 14.31% and 21.84% respectively, largely because the global economy has rebounded and demand for commodities has expanded.. The peak shipping season at the end of the year and the rise in the international raw material market, coupled with the implied boost in imports because of export demand, is expected to result in an increase in the output. It is estimated that growth of exports and imports in the whole of 2021 will be 16.78% and 18.57%, respectively. The rapid growth of digital business opportunities and application of emerging technologies will help maintain the momentum of exports next year. However, international logistics and supply chain issues do imply increased uncertainty in foreign trade. Considering the high growth in the base period, and after taking into account the price factor, it is expected that exports and

imports of real goods and services in 2022 will grow 3.41% and 2.77% respectively.

Inflation has moved up because of rise in energy and raw materials prices. The Consumer Price Index (CPI) increased by 1.91% from January to November on average over the same period last year, while the core consumer price index was up 1.28% during the same period. The wholesale price index (WPI) has gone up because of imbalance between supply and demand in the energy market caused by volatility in consumption of several countries. This has led to an increase in energy prices, and prices of bulk commodities have also risen due to shortages of raw materials caused by logistics and transportation issues. In the first 11 months, the wholesale price index (WPI) has risen 9.13% compared with the same period last year. As the base is low, CPI and WPI for the whole of 2021 are expected to rise 2.01% and 9.55% respectively. The global inflation problem will continue next year, and the significantly higher wholesale price index is expected to impact consumer prices. Attention should be paid to the delayed effect of consumer prices. After a period of time, the increase in manufacturers’ production costs will be passed on to the consumer. CPI and WPI are expected to rise 2.04% and 4.04% respectively in 2022.

Unemployment rate in the first 10 months of this year was 4.02%. In the second half of the year it decreased month by month, reflecting the gradual improvement in the labor market. However, some service industries are still facing adverse effects of the epidemic. It is expected that unemployment rate in 2021 and 2022 may decline marginally to 3.98% and 3.85%. In 2021, under a loose monetary policy, M1B and M2 are expected to maintain annual growth rates of 16.36% and 8.73% respectively. However, in the face of a rising inflation, major central banks around the world are starting to tighten monetary policies, affecting the domestic capital market. Under the high base period, M1B and M2 growth is expected to be 6.21% and 6.31% respectively in 2022.

Looking ahead, apprehensions about the risk of new variants of the virus have resulted in several countries taking anti-epidemic steps again and this has led to delays in trade and transportation and lack of labor, besides affecting import and export trade and commodity supply chains. Disruptions in global supply chains has led the IMF and OECD to slightly lower the GDP forecasts for major economies and increase forecasts of inflation. This shows an increase of the uncertainty of economic recovery. Geopolitical risks such as trade disputes between the United States and China and competition in key global supply chains are also likely to affect the growth of Taiwan’s foreign trade. In addition, consumers are facing increasing inflationary pressures as well as volatility of financial markets caused by tightening of hitherto loose monetary policies. Given the aforementioned factors and prediction errors, the 50% interval forecast for Taiwan GDP growth in 2022 will range from 2.77% to 5.06%.