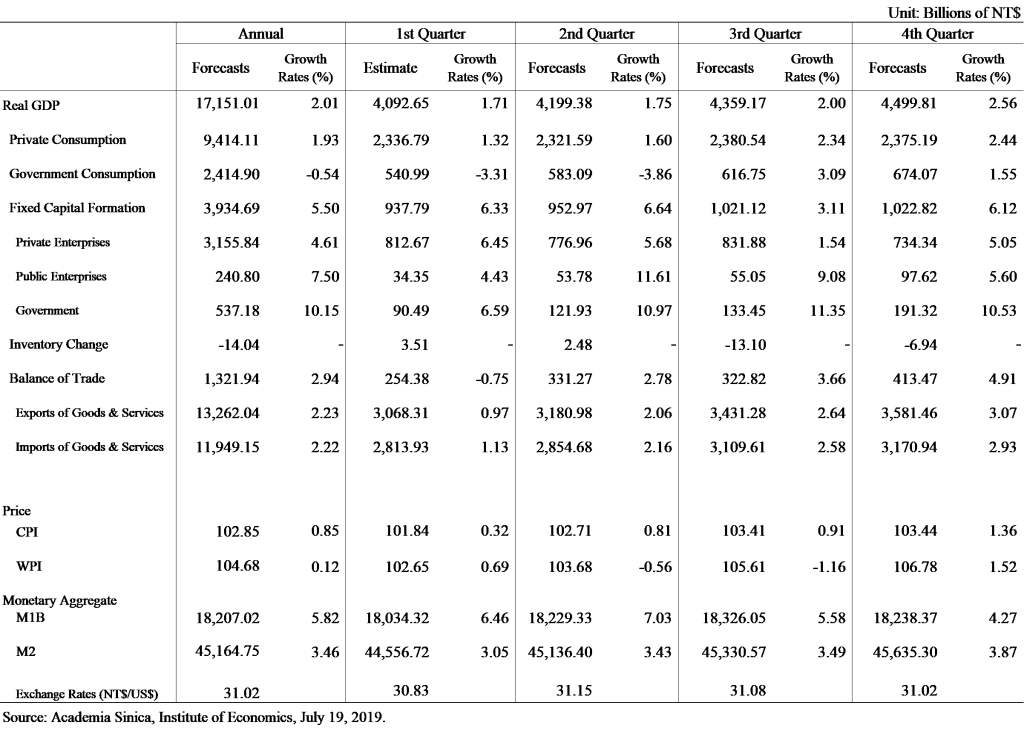

In the wake of continued trade disputes between the United States and China, global manufacturing output and world trade volumes have plummeted sharply. This has made the trend of slowdown in global economic growth more apparent in the first half of 2019. Taiwan too is experiencing declines in export orders, exports and industrial production because of the global economic downturn. The sluggish export and slump in consumption has led to Taiwan’s real GDP in first quarter of 2019 growing by only 1.71%, a decline on a quarter-on-quarter basis. Amid the economic headwinds intensified by high tariff barriers, the pressure on external trade has remained high and therefore, we have lowered our 2019 GDP growth forecast to 2.01%.

Real growth of private consumption was 1.32% (year-on-year) in the first quarter, showing a markedly weak growth in consumption, attributed to decrease in consumption of durable goods, motor vehicles, electronic products and home appliances. Additionally, the cumulative turnover of wholesale, retail and catering trades from January to May decreased by 1.43%, corroborated by the declining sales of the wholesale industry. Stagnant demand for overseas trade and related production activities also offset the rise in revenue of retail and food sectors. This shows that consumption is weakening. Nonetheless, the latest Taiwan Consumer Confidence Index (CCI) was on the rebound; the government’s incentive package and firms’ improved willingness to raise salaries would help private consumption grow moderately. After taking into account the price factors, real private consumption is projected to grow by 1.93% in 2019.

Benefiting from considerable imports of capital equipment by the semiconductor industry, real private investment grew by 6.45% (year-on-year) in the first quarter, which contributed to manufacturing fixed asset investment growth of 29.8%. With the active repatriation by Taiwanese companies, annual growth of capital equipment imports (in US dollars) in the first half of this year has reached 15.8%. Under successive adjustments to production lines by companies in response to the trade situation, real private investment is expected to grow by 4.61% (year-on-year) in 2019. The real fixed capital spending is also estimated to grow by 5.50% year-on-year, with rising contributions from government and public investments.

On the external trade front, real exports of goods and services grew slightly by 0.97% (year-on-year) in the first quarter of 2019, while real imports of goods and services also increased by 1.13% (year-on-year) during the same period. This was largely due to the knock-on effect of the escalating U.S.-China trade war and the slowdown of China. Merchandise exports were down for the seventh consecutive month in May, though there was a temporary rebound in the month of June due to the order-transfer effect of the trade war. However, the rate of recovery was still limited. This caused the average monthly growth over the first half of this year in exports and imports (in US dollars) has been -3.38% and 0.06%, respectively, reflecting a fading momentum in external sector. Recently, Taiwanese manufacturers’ plans to increase the proportion of their global capacities in Taiwan, as well as emerging business opportunities, such as expansion of 5G communications and artificial intelligence, are expected to offset some of the negative impact in the second half of this year. Consequently, we expect that both exports and imports of goods and services shall remain stagnant (2.23% and 2.22% growth) in 2019.

Because of the edging up of food price and the phasing out of cigarette tax, the consumer price index (CPI) increased by 0.56% in the first six months of 2019. The core CPI grew by 0.49% in the same period while the wholesale price index (WPI) rose only 0.05% as commodity prices have slightly decreased since the beginning of the year 2019. In consideration of the decline in raw material prices and a fluctuation on international oil price because of political risks and extension of OPEC production cuts, annual CPI and WPI are both estimated to remain relatively moderate, with 0.85% and 0.12% growth (year-on-year) respectively in 2019.

The labor market has apparently stabilized as the average unemployment rate in the first five months was 3.67%. Considering a tight labor market and an increase in minimum wage, we expect unemployment rate in 2019 to remain steady at around 3.70%. However, the economic slowdown leads to doubts about labor demand sustaining in coming months. With acceleration of FDI inflows into the buoyant stock market, M1B expanded 6.85% (annualized) in the first five months of 2019, while M2 increased at an annualized rate of 3.25%, indicating ample market liquidity to support economic activity. The domestic demand for capital may rise because of investments by local companies. In 2019, M1B and M2 are projected to be up by 5.82% and 3.46% respectively.

Looking into the future, the latest reports from the IMF and the World Bank predict slower growth for the global economy and world trade volume in 2019, indicating that the economic growth is worse-than-expected. U.S. and China have imposed tit-for-tat tariffs on each other and that has already affected global supply chains, implying greater challenges for companies. We still need to pay more attention to subsequent developments as trade tensions may get intensified. Lower volumes of production and trade may result in reducing investment. These developments may affect consumer confidence and corporations’ willingness to invest. Additionally, the increasing uncertainties about the probability of growing trade protectionism, vulnerability of international financial markets and geopolitical tensions, the economy is likely to remain fragile. Even though expectations of a trade truce and the Fed’s rate cuts leave us positive over prospects, the severe external trade environment still weighs on business conditions. As for Taiwan, with the government incentive program, returning investment has been setting a new record. With fiscal stimulation for domestic consumption and tax reform, as well as positive signs on transfer of US orders from China to Taiwan, these initiatives would boost domestic demand and cushion the effect of the weaker trade outlook, which may strengthen Taiwan’s economic growth in the second half of the year. However, the latest manufacturing PMI signals further contraction, showing a weak outlook and calling for caution on corporate investment. Besides implementation of the relevant policies by the government, such as those aimed at boosting investment, forward-looking infrastructure development program, and energy transformation, should continue to inject some degree of optimism. Taking all factors into account, we expect that the 50% confidence interval of real GDP growth will range from (0.92%, 3.21%).

2019 Taiwan Economic Forecast: A Revision